The Dose

Strategic intelligence for life science consulting

Issue 001 · June 2026

Executive Summary

Three forces are reshaping life sciences in 2026.

First

The clinical API layer is emerging as a standalone asset class - OpenEvidence's $12B valuation is the clearest proof point yet.

Second

Capital is moving earlier and faster in biology-x-AI, with Series A rounds reaching sizes that once required Phase II data.

Third

Regulatory risk is being systematically mispriced in investor decks - Galera's CRL is the latest reminder that Breakthrough designation is a signal of FDA interest, not a guarantee of approval.

This issue covers all three, with a presentation lens built for life science consulting teams.

01 · The Signal

One structural shift. Explained clearly.

Medical intelligence is separating from the application layer - and it's quietly rewriting the rules of how healthcare software gets built and sold.

OpenEvidence just raised at a $12 billion valuation. It doesn't own a hospital. It doesn't run an EHR. What it does is package clinical intelligence and make it available through an API so any physician workflow, agent, or platform can simply plug in and use it.

That structural fact is more interesting than the number. OpenEvidence doesn't have one patient relationship to show for its twelve billion dollar valuation. No workflow ownership, no doctor loyalty, nothing like that. Just an intelligence layer that's validated, API-ready, and quietly sitting inside products that do have all those relationships. Turns out owning the layer underneath is more valuable than owning the front door.

"The companies creating clinical intelligence no longer need to own the customer relationship. The companies owning the customer relationship no longer need to build the intelligence. That separation is what is changing the economics of healthcare software."

A growing number of companies are making the same structural move. Corti ships inside telehealth platforms. Suki is embedded inside athenahealth. AMBOSS exposes its medical knowledge through MCP endpoints for AI agents to call. Infermedica, Abridge, Aidoc, Glass Health - different products, different buyers, same underlying bet.

What this means for you: If you're building in clinical AI, the first question any serious investor will ask is which layer you sit in. Make sure you have a clear answer before that conversation happens. If you are pharma or a health system: the build vs. buy vs. embed decision just became strategic. If you are raising: your competitive landscape slide needs to address this stack. Decks that ignore it look behind the curve.

02 · Funding Pulse

Notable rounds, deals, and capital movements

$4.1B total · 14 rounds tracked · 3 deals above $300M

OpenEvidence · $12B valuation · Growth round

AI-powered medical search for clinicians. Raised $250M Series D led by Thrive Capital and DST Global. Used by 40% of US physicians. Revenue crossed $100M ARR.

Xaira Therapeutics · $1B · Series A

AI-native drug discovery platform co-incubated by ARCH Venture Partners and Foresite Labs. Led by former Stanford president Marc Tessier-Lavigne. One of the largest Series A rounds in biotech history. The bet: AI can design previously undruggable proteins in weeks.

Waystar · $968M · IPO (Nasdaq: WAY)

Healthcare payment software. Largest health tech IPO since 2022. Backed by EQT, CPPIB, and Bain Capital. $791M in 2023 revenue. Strong signal that the health tech IPO window is reopening after a two-year freeze.

Nuvation Bio · $200M · Series D

Precision oncology company focused on next-generation cancer therapies.

Inato · $103M · Series C

Clinical trial site network platform. Connecting sponsors with global trial sites faster.

Cartography Biosciences · $60M · Series B

Oncology target discovery using single-cell genomics to identify cancer-specific targets.

03 · Pipeline Watch

Regulatory decisions, trial readouts, and approvals

Vertex Pharmaceuticals - Alyftrek (vanzacaftor/tezacaftor/deutivacaftor)

FDA approved Dec 2024. Once-daily CFTR modulator for cystic fibrosis. Covers F508del + 31 mutations. Vertex's fifth CFTR approval.

Sanofi - Qfitlia (fitusiran) for Haemophilia A and B

FDA approved Mar 2025. First therapy for all haemophilia A & B regardless of inhibitor status. 6 injections/year. $1B potential by 2030.

Relay Therapeutics - Zovegalisib (RLY-2608)

Breakthrough Designation Feb 2026. PI3K inhibitor for HR+/HER2- breast cancer (PIK3CA). Cleaner tolerability vs. pan-PI3K. Phase III enrolling.

AstraZeneca - Tagrisso + datopotamab deruxtecan (TROPION-Lung08)

First-line EGFR-mutated NSCLC. TROPION-Lung01 met dual primary PFS vs. docetaxel. First-line combo data could redefine standard of care.

Galera Therapeutics - GC4419 (avasopasem)

CRL Aug 2023. ROMAN trial data not persuasive for oral mucositis. Additional trial required. Note: Fast Track + Breakthrough designation does not guarantee approval.

KEY SIGNAL: Two approvals in CF and haemophilia signal sustained investment in rare disease. Breakthrough designation does not guarantee approval - a distinction worth a slide of its own in any regulatory deck.

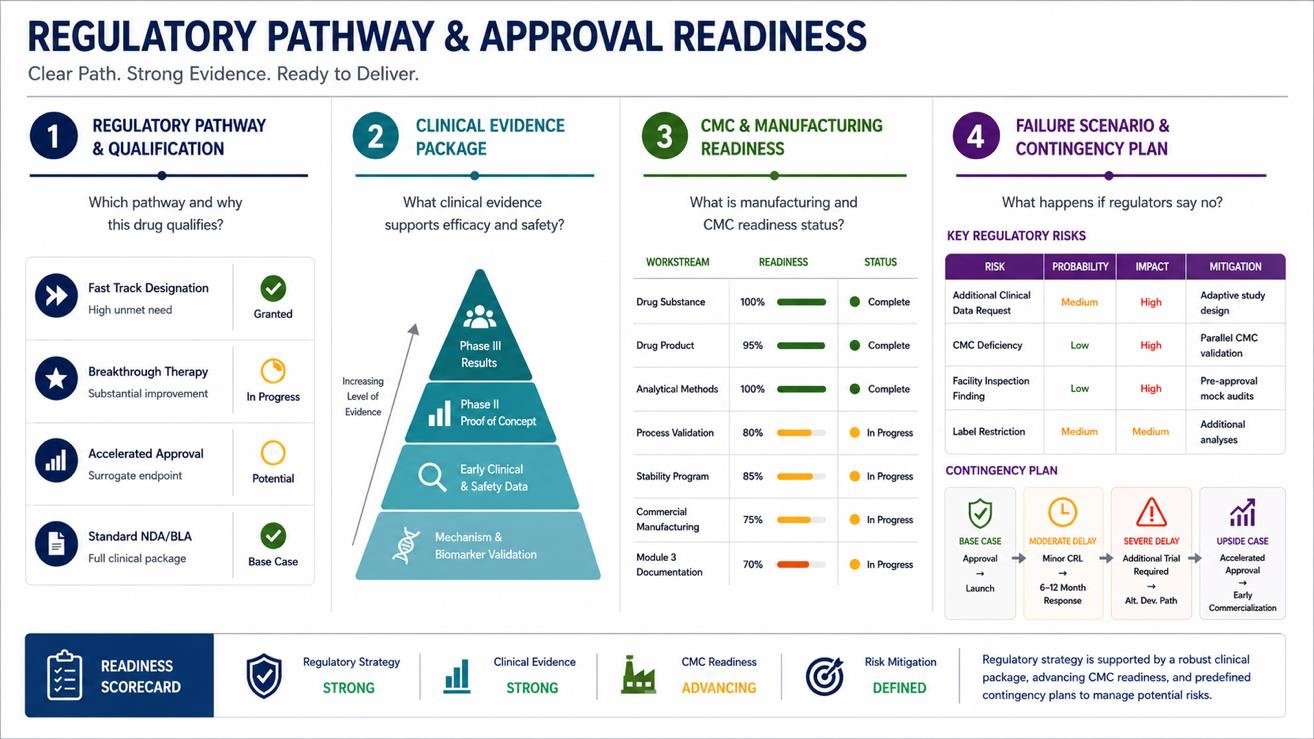

04 · The Deck

One presentation insight tied to this issue's news

Galera's CRL was not about the science. The clinical data had compelling precedent the drug held Breakthrough Therapy designation. The failure was that the totality of evidence was not considered persuasive enough by the agency to establish substantial efficacy. This is a different kind of failure than a manufacturing defect, and it points to a presentation challenge: how you sequence and frame clinical evidence matters as much as the data itself.

Your regulatory slide needs to answer four questions - not one. Most regulatory slides answer question one and stop. Investors who have been through a CRL will probe all four: Which regulatory pathway and why this drug qualifies; what clinical evidence supports the efficacy and safety case; what the manufacturing and CMC readiness status is; what the failure scenario looks like and what the contingency plan is.

05 · Editor's View

Perspective from the desk

The clinical API layer is most interesting. It has traditionally been believed that power and value come from owning the workflow. For the first time, clinically relevant and validated intelligence has emerged as a standalone asset that can be integrated across platforms, providers and different care settings (tertiary/primary). I believe this is a trend to stay and further evolve and mature with usage. In healthcare settings, it's often difficult to scale clinical expertise. If AI can genuinely deliver evidence-based guidance accurately with an accuracy ratio of over 90% at the point of care, its impact on efficiency, decision-making, and patient outcomes would be significant.

Healthcare is not like other industries where a good product finds its users. Here, a product has to survive MLR review, pass clinical validation, earn a place inside a regulated workflow, and then convince a physician who carries personal liability for every decision - to actually trust it. That is four separate adoption barriers before a single patient is impacted.

A $12B valuation and a 90% accuracy benchmark do not move the needle on physician adoption. What does: real-world evidence generated in the clinical environments where the tool actually runs, integration that fits inside existing workflows rather than adding a new one, and a regulatory framework that gives physicians cover to act on AI guidance. Heading into H2 2026, those three conditions - not valuation, not model performance - are what I will be watching.

The clinical API layer is real, but the adoption story is not keeping pace with the valuation story. Healthcare has four barriers no other industry has - regulation, clinical validation, workflow integration, and physician trust - and none of them yield to a strong funding round. Heading into H2 2026, real-world evidence and regulatory clarity will separate the genuine platforms from the well-funded experiments.

06 · Further Reading From A1Slides

Insights on presenting in life sciences and high-stakes environments

NEWSLETTER

Stay Ahead in Enterprise Communication

Get insights, research, and decision-design best practices for leaders.